Your Budget Has Four Pillars (And You're Probably Ignoring Two of Them)

Kakeibo budgeting provides simplification and alignment.

Every budgeting app I’ve ever used organizes your money the same way: categories. Groceries, rent, utilities, dining out, entertainment, subscriptions, “miscellaneous.” You get fifty categories and a pie chart that looks like a bag of Skittles exploded on your screen. Very colorful. Completely useless for actually understanding what your money is doing.

The problem isn’t the categories themselves. Categories are fine for tracking where money went. The problem is that categories don’t tell you why you’re spending it, and they definitely don’t tell you whether your spending reflects the life you’re actually trying to build.

That’s where Kakeibo comes in. And that’s why Heartfelt Finance doesn’t organize your budget by category (I mean, yeah, it does, but at a micro level). At a macro level, it organizes by pillar.

What Kakeibo Got Right in 1904

Kakeibo is a Japanese budgeting method that dates back to 1904, invented by Hani Motoko, Japan’s first female journalist. The core idea is disarmingly simple: instead of tracking fifty spending categories, you sort your money into four buckets based on the role it plays in your life.

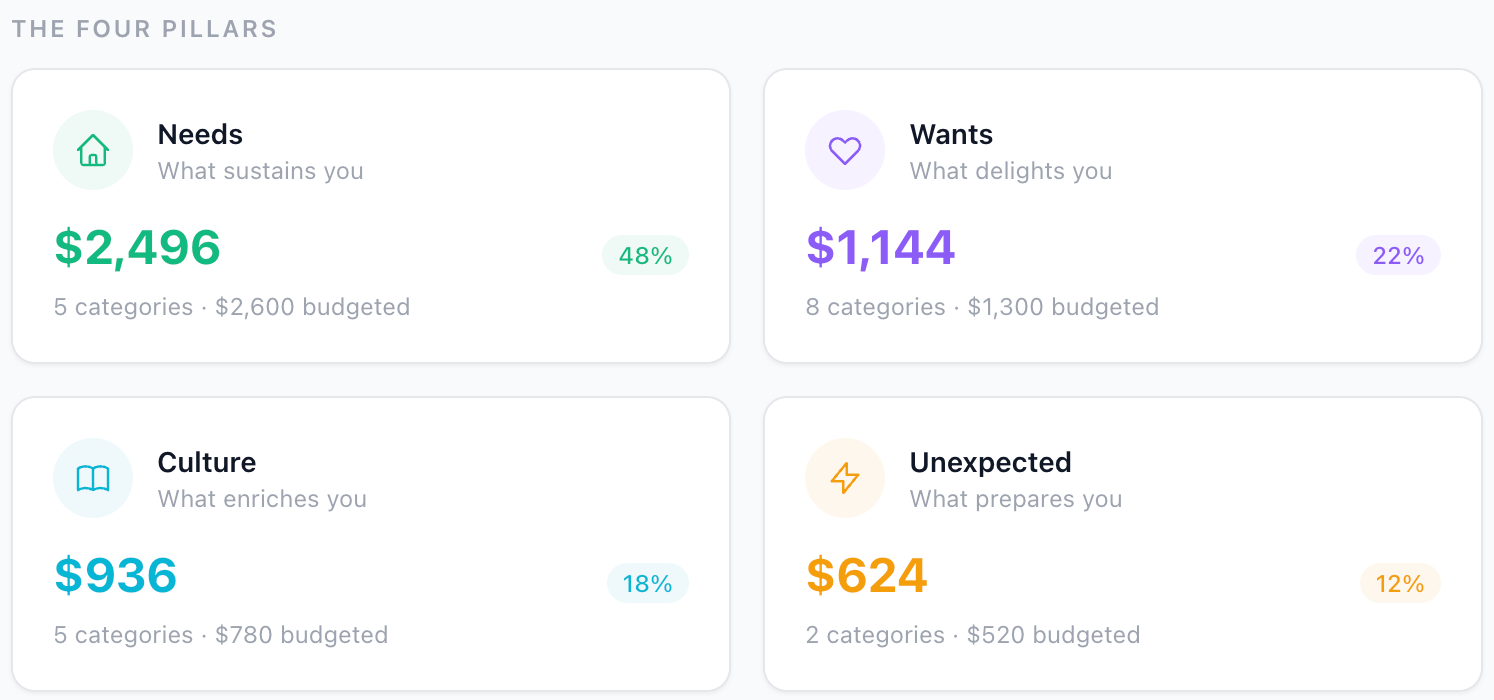

Needs. What sustains you. Shelter, food, health, transportation, insurance. The non-negotiables that keep your life functioning. You don’t feel guilty about Needs. You honor them, because knowing your true baseline cost of living is the foundation of every other financial decision you’ll ever make.

Wants. What delights you. The streaming subscription, dinner with friends, the new shoes you’ve been eyeing. Wants aren’t the enemy. They’re the whole reason you work. The practice isn’t to eliminate them; it’s to choose them deliberately instead of accumulating them on autopilot.

Culture. What enriches you. Books, courses, museum memberships, music lessons, charitable giving, the yoga workshop, the conference ticket. This is where it gets interesting, because almost no Western budgeting system has a category for “things that make you a more complete human being.” They lump it all into “entertainment” or “miscellaneous” — as if a $15 book on stoic philosophy and a $15 impulse buy at Target are the same kind of spending. They’re not.

Unexpected. What prepares you. The car repair, the medical copay, the appliance that dies three months after the warranty expires. Every budget has an emergency fund line item. Almost no budget has a philosophy about the unexpected. Kakeibo does: life will surprise you. Build the buffer that lets you meet surprise with calm instead of panic.

The Two Pillars Nobody Talks About

Here’s what I noticed after years of using traditional budgets: I could account for every dollar and still feel like something was off. My spreadsheet said I was doing fine. My gut said I was treading water.

The missing piece was Culture and Unexpected.

In a traditional budget, my $145 vocal lessons go under “Entertainment.” My $165 in books and courses went under “Education” or, more likely, “Miscellaneous.” My charitable giving went under... honestly, it went wherever I remembered to put it that month. All of that enrichment spending — over a thousand dollars a month that was actively making my life better — was scattered across half a dozen categories, invisible in the aggregate.

Meanwhile, my emergency fund contribution sat in “Savings” right next to my vacation fund and my house down payment, as if preparing for a blown transmission and planning a trip to Japan serve the same emotional function. They don’t. One is defense. The other is aspiration. Treating them identically means you never see how well you’re actually prepared for the curveballs.

When I reorganized everything into four pillars, two things jumped out immediately. First, I was spending more on Culture than I realized — and that was good. That spending was intentional, enriching, and aligned with who I want to become. Second, I was spending almost nothing on Unexpected, which meant every actual emergency sent me scrambling.

The four-pillar view didn’t change how much money I had. It changed what I could see.

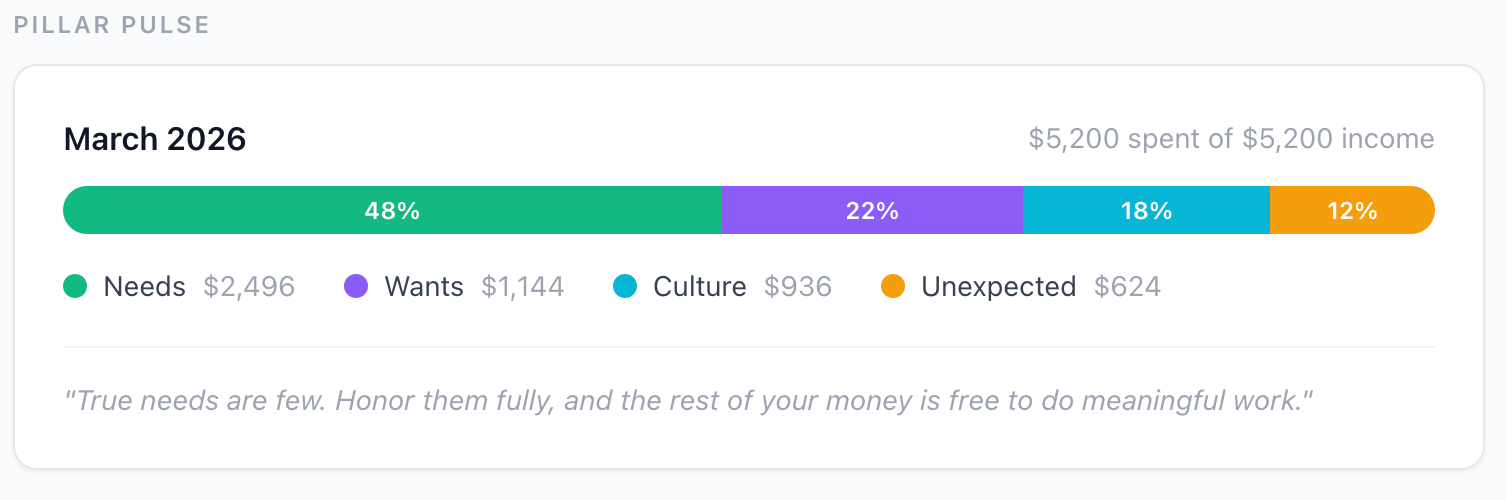

What the Pillar Pulse Reveals

Heartfelt Finance shows your four-pillar distribution as a horizontal bar called the Pillar Pulse. It appears on your dashboard and your budget plan page. Four colors, one bar. Your entire financial month compressed into a single visual.

There’s no “right” ratio. A grad student’s Pillar Pulse will look nothing like a mid-career professional’s, and both can be perfectly healthy. The point isn’t to hit some magic percentage. The point is to see the balance — or imbalance — clearly enough to make a conscious decision about it.

When Wants starts creeping up to 35% and Culture drops to 5%, that’s a signal.

Not a moral failing. A signal.

It means your money is flowing toward consumption and away from growth. Maybe that’s fine for a month or two. Maybe it’s a pattern worth examining. The Pillar Pulse makes the pattern visible so you can decide for yourself.

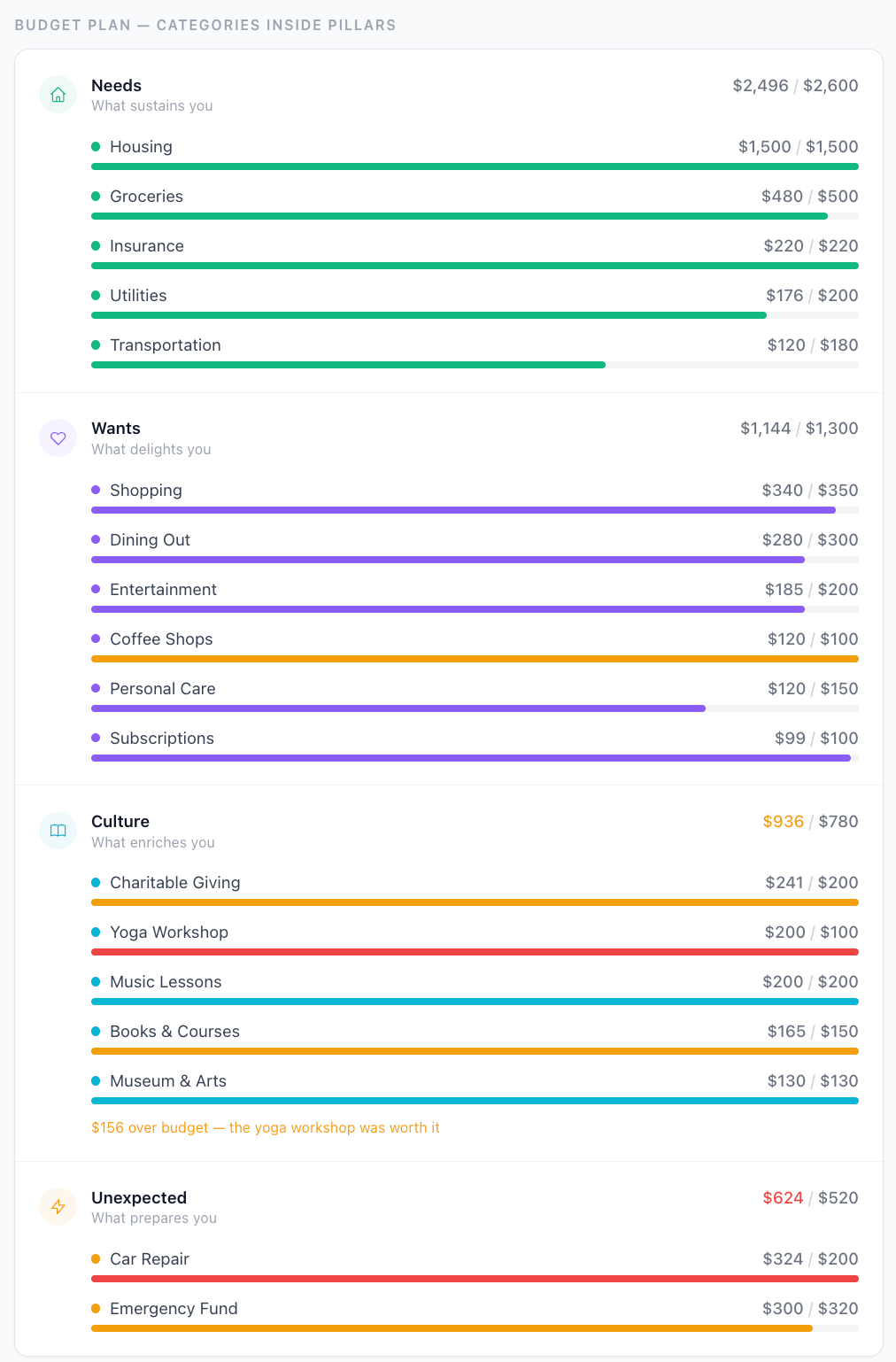

Budget Plan: Categories Inside Pillars

This is where Heartfelt Finance diverges from every budgeting app I’ve used. Instead of showing you a flat list of fifty categories, the budget plan groups your categories under their pillar. Needs at the top, then Wants, then Culture, then Unexpected. Each pillar shows its total allocation and spending, and each category within it shows its own progress bar.

The visual hierarchy matters more than you’d think. When your categories live inside pillars, you stop seeing “Groceries: $480” in isolation and start seeing “Groceries: $480, which is part of Needs, which is 48% of my total budget.” Context changes everything. That $480 grocery bill feels different when you can see it’s a fraction of a well-structured foundation versus half your entire budget.

Every category gets assigned to exactly one pillar. You make that decision once — when you create the category — and then every transaction that lands in that category automatically feeds the right pillar. No extra tagging, no extra clicks. The structure does the work for you.

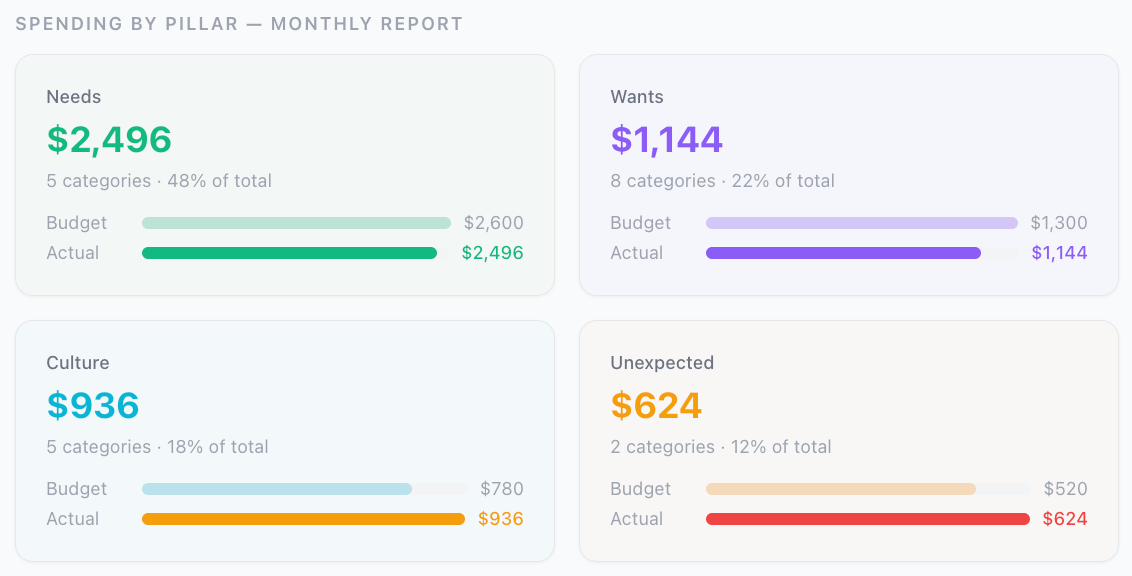

The Spending Report: Four Cards, One Story

At the end of the month, the Reports page shows you a spending-by-pillar breakdown. Four cards, each tinted with the pillar’s color, each showing exactly how much you spent, how many categories contributed, and how it compared to what you budgeted.

Below the cards, comparison bars show allocated versus actual for each pillar. Green when you’re under budget, amber when you’re close, red when you’ve blown past it.

The four-card layout forces a different kind of analysis than a category pie chart. Instead of asking “did I spend too much on dining out?” you ask “is the balance between what sustains me, what delights me, what enriches me, and what prepares me roughly where I want it to be?” That’s a fundamentally better question. It’s a question about your life, not your line items.

Why This Works

I’ve tried every budgeting methodology that exists. Envelope system, zero-based, percentage-based, the 50/30/20 rule, YNAB’s “give every dollar a job” approach. They all work mechanically. You can follow any of them and end up with a functional budget.

The four-pillar system works *psychologically*. It doesn’t just tell you where your money went. It tells you what your money did. Did it sustain you? Did it delight you? Did it enrich you? Did it prepare you? Four questions, four honest answers, and suddenly you understand your financial life at a level that no category breakdown can reach.

Hani Motoko figured this out in 1904. It took American personal finance about 120 years to catch up. Heartfelt Finance is my attempt to close that gap with software instead of a paper ledger, but the insight is the same one she had: your budget is a portrait of your priorities. Make sure it’s painting the picture you actually want.

Set up your four pillars. Assign your categories. Spend one month watching the Pillar Pulse. I guarantee your money will tell you something about your life that fifty categories never could.

Heartfelt Finance is free for individual users. It’s a budgeting tool, spending tracker, goal planner, credit score education tool, and the like — but built around money mindfulness. Check it out at https://HeartfeltFinance.com.