The $0 Financial Plan That Beats a $300/Hour Advisor

Put that money towards paying down debt instead.

Let me tell you what a financial advisor actually does in the first session with you. They ask you what you earn, what you owe, and what you want to do with your money. Then they write it down. Then they charge you for the hour.

That’s not cynicism — that’s the process. And the uncomfortable truth is that most people who hire a financial advisor at $200–$300 per hour don’t need an advisor. They need a system. There’s a difference.

I’m not saying advisors are useless. A good CFP earning her fee is worth every penny when you’ve got a complex estate situation, a pension decision to make, or a tax problem that requires genuine expertise. I’m talking about the other 80% — the people who walk into an advisor’s office carrying $14,000 in credit card debt and a vague sense that they should probably be saving more. Those people don’t need a fiduciary. They need a budget and a debt payoff sequence, and they can build both themselves for exactly zero dollars.

Here’s the plan.

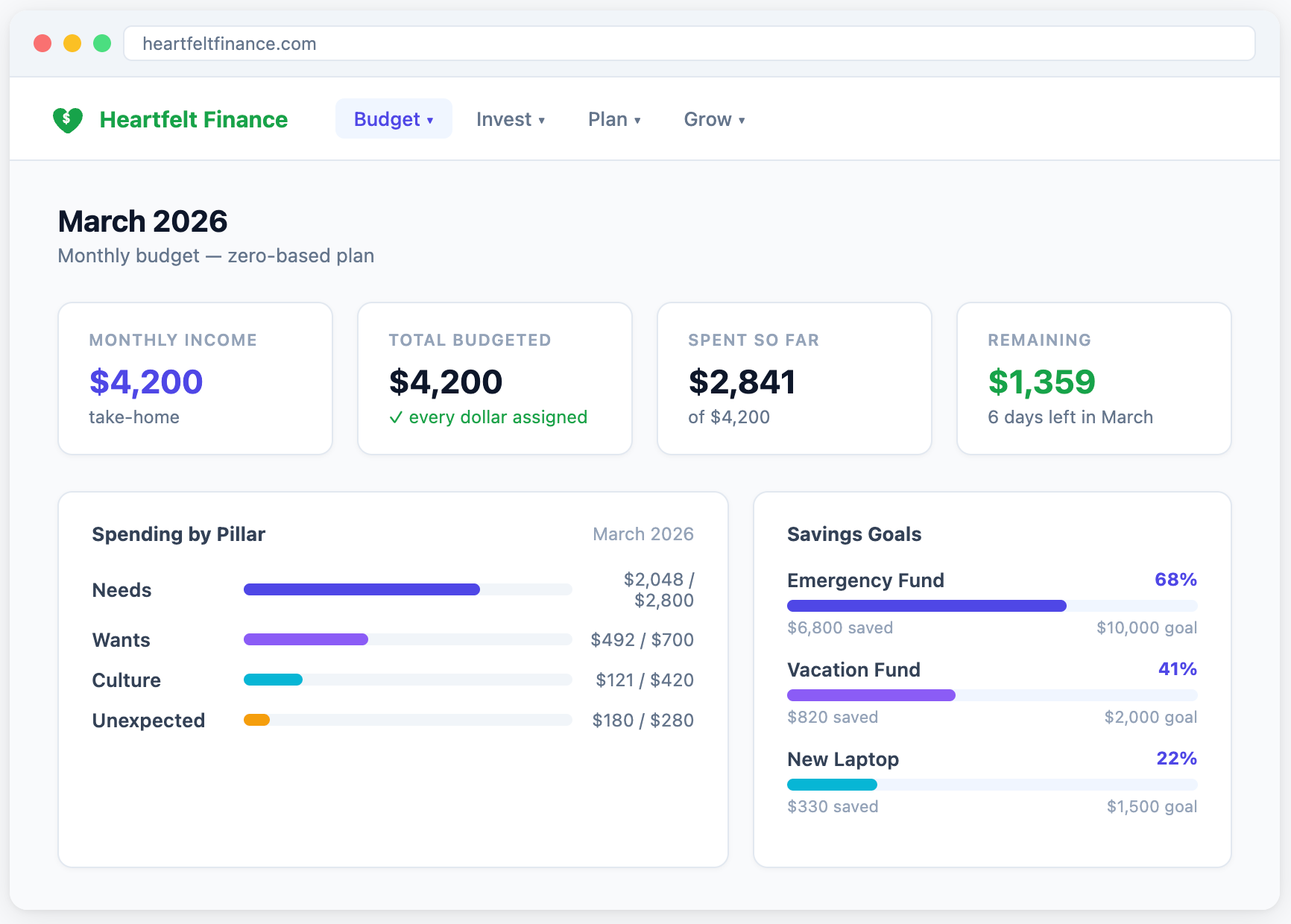

Step one: Every dollar gets a job

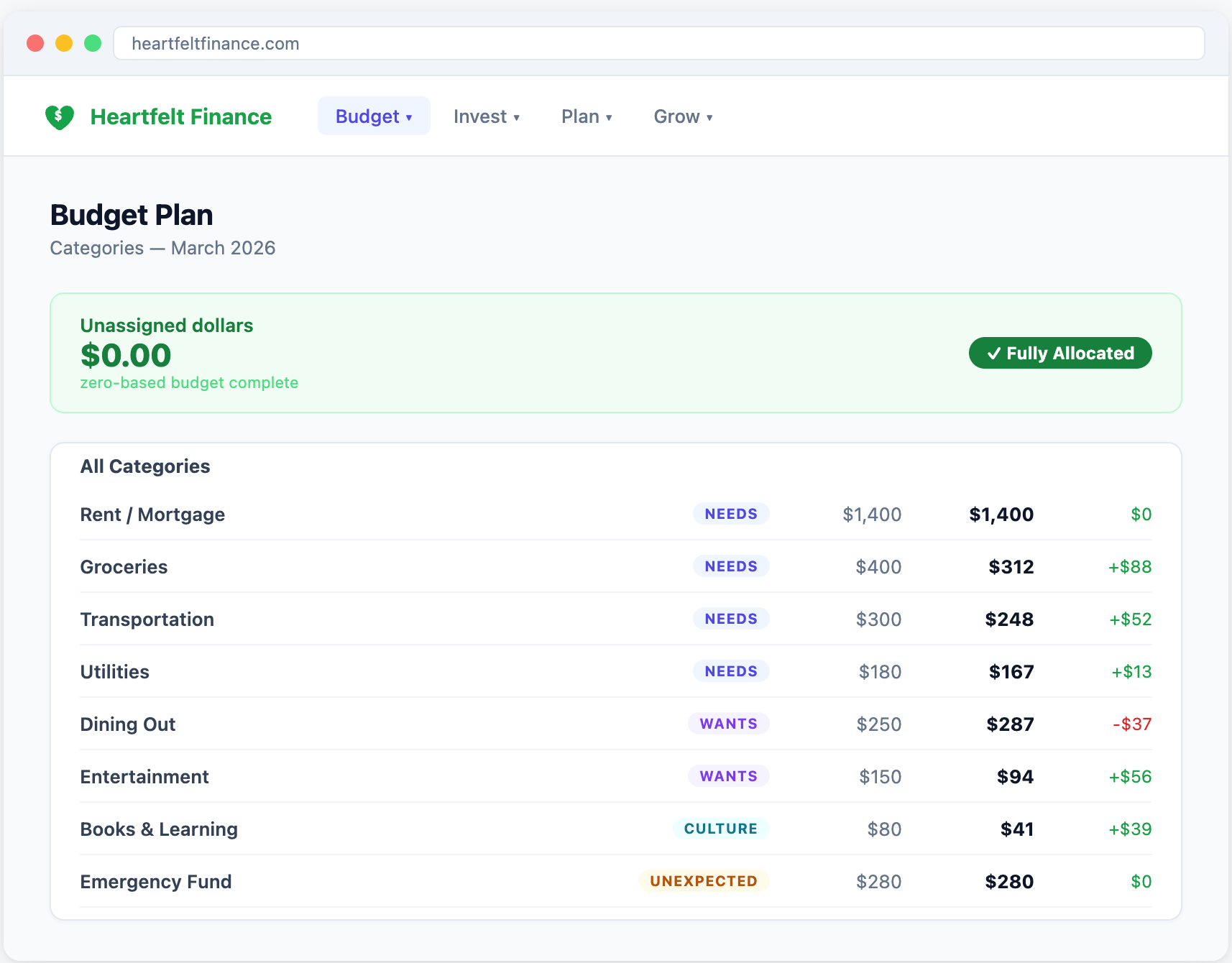

Zero-based budgeting is the foundation, and the concept is simple. Your income minus your expenses equals zero — not because you’ve spent everything, but because every dollar has been assigned somewhere intentional. Savings is an expense. Debt payoff is an expense. Entertainment is an expense. The point is that nothing goes “wherever” at the end of the month, because “wherever” is the enemy.

I use a Kakeibo-inspired four-pillar structure — Needs, Wants, Culture, and Unexpected — because it forces you to categorize spending by purpose rather than by vendor. Knowing that you spent $287 at restaurants is useful data. Knowing that $287 went toward Want-category spending when your budget was $250 tells you something you can actually act on.

Step two: Know where you stand

Before you can build the plan, you need the numbers. Monthly take-home income, a list of every debt (balance, APR, minimum payment), and a rough tally of what you spend each month by category. That’s it. You don’t need a net worth statement on day one. You don’t need projected returns on a portfolio you haven’t built yet.

The thing most people skip is writing it down. Actually putting the numbers somewhere forces you to confront them. I’ve watched people’s jaws drop when they first do a budget and realize their minimum payments alone are eating 22% of their take-home pay. The advisor doesn’t do that to you — the numbers do.

Step three: Build the payoff sequence

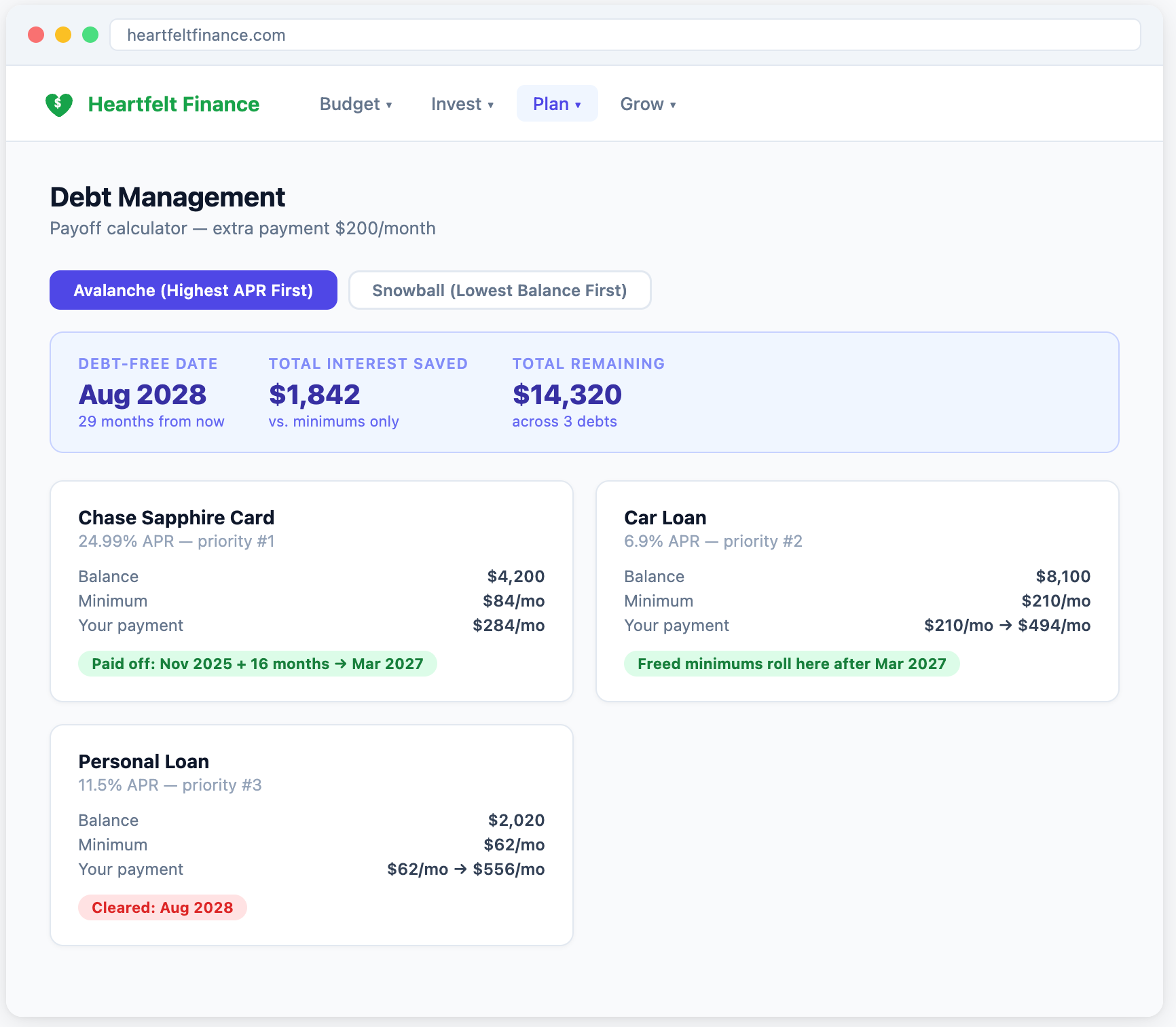

Two methods. Avalanche: pay the highest APR debt first, throw every extra dollar at it until it’s gone, then roll that payment to the next highest. This minimizes total interest paid. Snowball: pay the smallest balance first, regardless of APR, to get quick psychological wins. The math favors avalanche; the psychology sometimes favors snowball. Pick the one you’ll actually stick to.

The key mechanic — the one that makes this work — is the roll. When debt #1 is gone, you don’t pocket that minimum payment. You add it to the extra you’re already throwing at debt #2. Freed minimums cascade. A $200 extra payment that clears a $4,200 credit card in 16 months becomes a $484 payment on the car loan the next day. That’s how you go from staring down $14,000 in debt to being debt-free in 29 months instead of seven years.

“But what about my 401k? My taxes? My investment strategy?”

I know what you’re thinking. “This is fine for people with simple situations, but I have real complexity.” Maybe you do. But I’d bet the that most of the people asking that question don’t have complexity — they have anxiety. There’s a difference.

Here’s a simple sequencing rule that covers 90% of situations: (1) contribute to your 401k up to the employer match — that’s an instant 50–100% return, take it; (2) pay off any debt above 7–8% APR aggressively; (3) max your Roth IRA; (4) invest the rest in low-cost index funds. No advisor required. John C. Bogle (the founder of Vanguard) said this forty years ago and the basic advice changed.

If you genuinely have a complex tax situation — multiple business entities, stock options, real estate, an inheritance — yes, hire someone. But be honest with yourself about whether the complexity is real or manufactured. The financial services industry profits from making normal money management seem complicated. It isn’t.

The $0 part

Heartfelt Finance is free. Zero-based budgeting, the four-pillar Kakeibo structure, savings goals, debt payoff simulation (avalanche and snowball), spending reports, values alignment — all of it is free. You don’t need a spreadsheet wizard, you don’t need a $15/month app subscription, and you definitely don’t need to hand $300 to someone to ask you what you earn.

If you are a financial consultant, coach, planner, advisor, or therapist, Heartfelt Finance has something for you, too. Head over to https://HeartfeltFinance.com/coaches to see how this tool can enhance your current practice.