Why I Built a Budgeting App That Asks You How You Feel

Every budgeting app on the planet will tell you that you spent $47.99 at Amazon last Tuesday.

Cool. Thanks. That and a dollar will get you a candy bar at the gas station (or maybe it’s two dollars, with inflation and all).

What no budgeting app will tell you is why you spent $47.99 at Amazon last Tuesday. Were you replacing a broken kitchen tool? Were you buying a birthday gift you’d been planning for weeks? Or were you doom-scrolling at 11pm after a brutal day at work and clicked “Buy Now” on something you can’t even remember ordering?

Those are three fundamentally different financial events. Your bank statement treats them identically. Your budget app categorizes them all as “Shopping.” And then everyone wonders why tracking expenses doesn’t actually change spending behavior.

That’s the gap I built the Mindful Tags feature inside the Heartfelt Finance app to close.

## Survival, Comfort, Escape

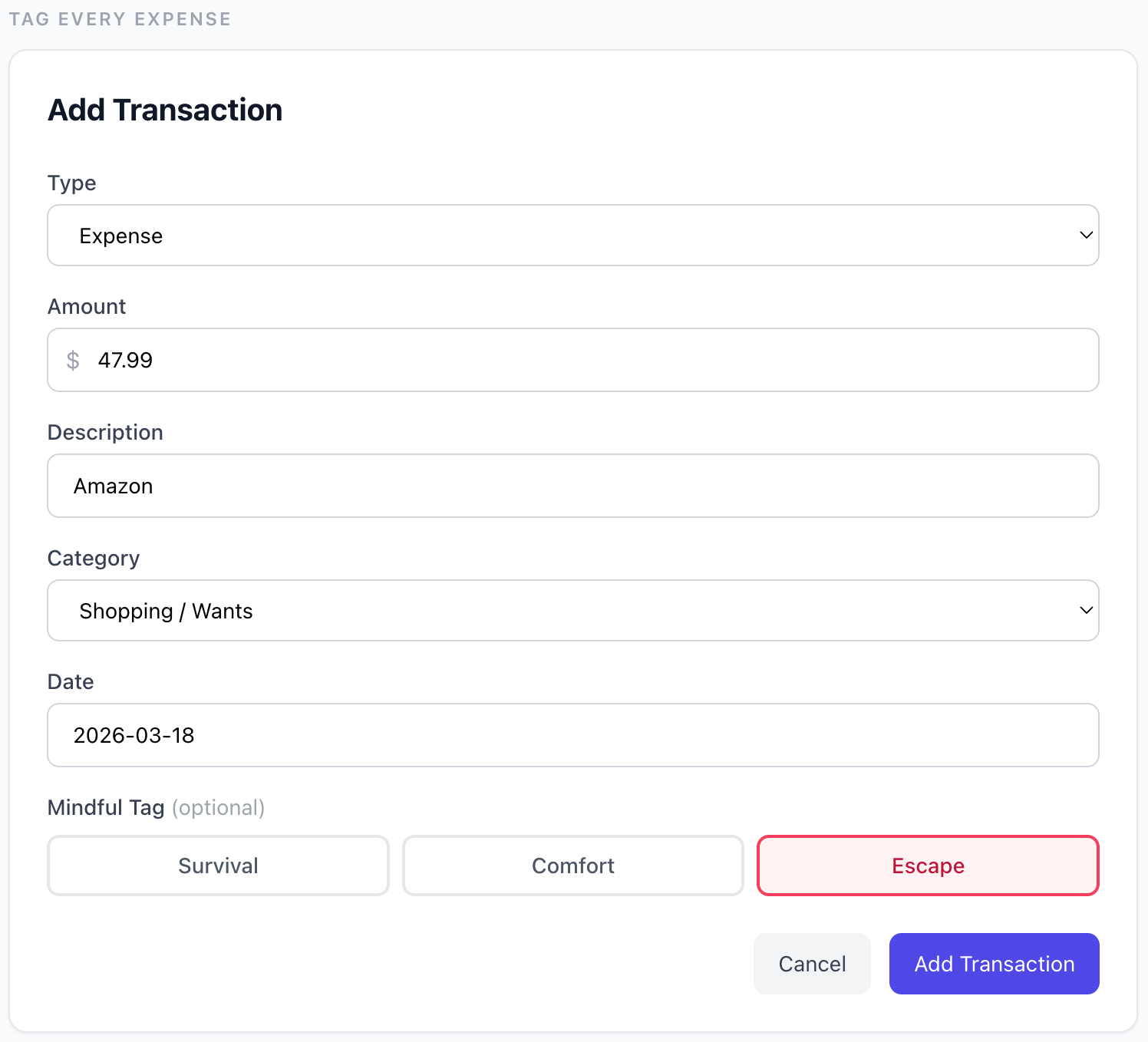

Heartfelt Finance asks you to tag every expense with one of three labels: Survival, Comfort, or Escape.

Survival is the stuff that keeps your life functioning. Rent, groceries, utilities, gas, insurance. You need these. They’re non-negotiable. The goal isn’t to feel guilty about them; it’s to honor them clearly so you know exactly what your baseline cost of living really is.

Comfort is the stuff that makes life enjoyable. Netflix, the yoga studio membership, a nice dinner out with friends, the Spotify subscription. Comfort spending isn’t bad. It’s the whole reason you work in the first place. The practice here is choosing it consciously rather than accumulating it unconsciously.

Escape is where it gets interesting.

Escape spending is the money you spend to avoid feeling something. The Amazon order after a fight with your partner. The DoorDash because cooking feels overwhelming tonight. The Target run where you walked in for paper towels and walked out with $67 worth of stuff you didn’t need and won’t remember buying by Friday.

Escape spending isn’t a moral judgment. It’s a data category. And until you can see it clearly, separated from the rest, you can’t make a decision about it.

The Three-Minute Tag

When you log an expense in Heartfelt Finance, three buttons appear below the amount: Survival, Comfort, Escape. One tap. That’s it. Takes about two seconds per transaction.

Over the course of a month, those two-second taps build a dataset that no other budgeting tool collects. Not “how much did you spend on groceries” — the answer to a fundamentally different question: *what was the emotional purpose of this money?*

Most people already know the answer in the moment. You know when you’re stress-buying. You know when you’re treating yourself intentionally versus numbing yourself reflexively. The tag just makes you say it out loud. Or, more precisely, it makes you tap a button that says it for you.

The act of categorizing is the intervention. Not the report you’ll look at later. Not the pie chart. The moment of honest classification, transaction by transaction, is where the behavior change happens. By the time you see the monthly breakdown, you’ve already been paying attention for 30 days.

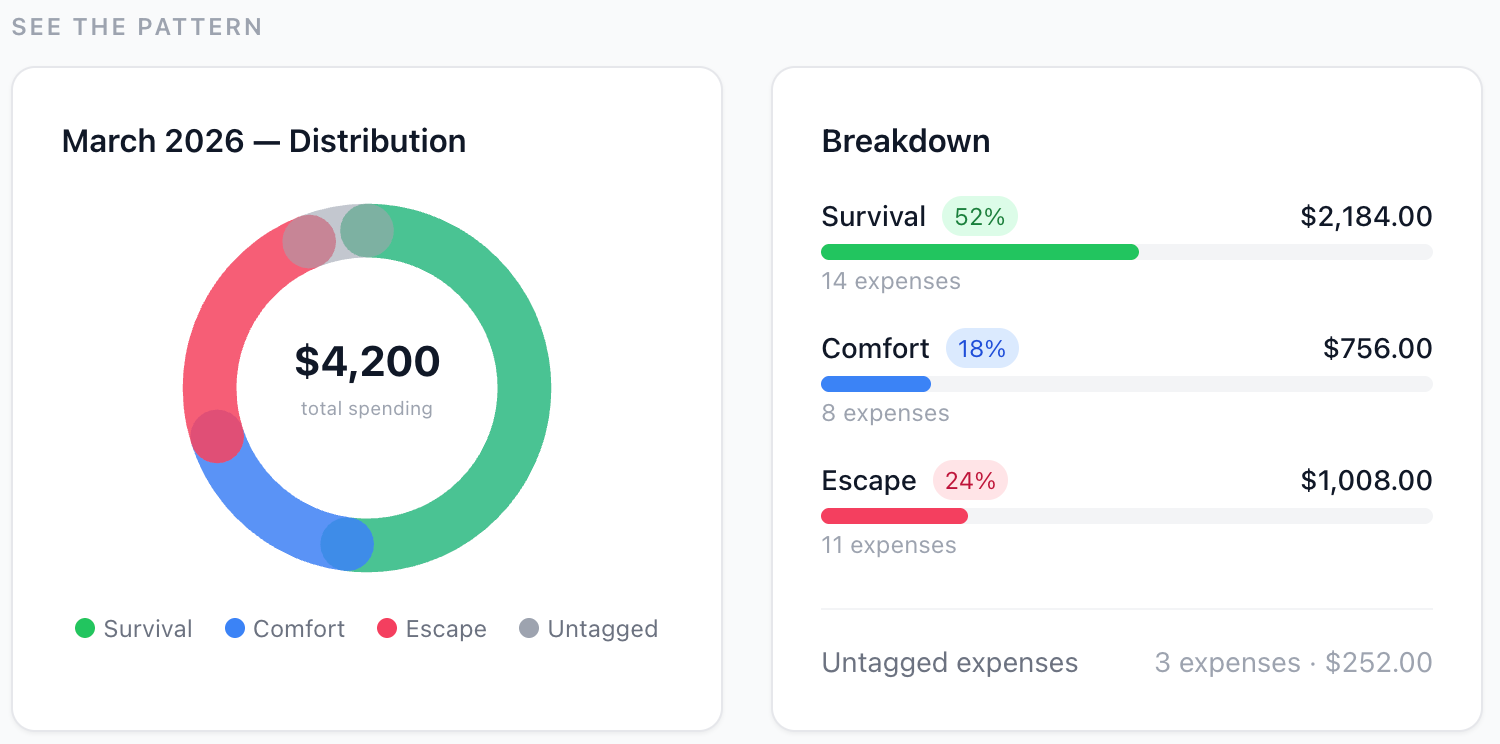

What the Donut Chart Reveals

At the end of the month, the Mindful Tags report shows you a donut chart. Three colors. Your entire month of spending, sorted not by category but by emotional intent.

Here’s what a real month might look like: 52% Survival, 18% Comfort, 24% Escape. That Escape number is the one that stops people cold. Twenty-four percent of discretionary spending going toward emotional regulation disguised as commerce. That’s over a thousand dollars a month for someone spending $4,200. Twelve thousand a year. The down payment on a house, evaporating into Amazon boxes and delivery fees.

Nobody set out to spend $12,000 a year on emotional avoidance. But without the tag, that number hides inside “Shopping” and “Food & Dining” and “Miscellaneous” — categories that tell you nothing about intent.

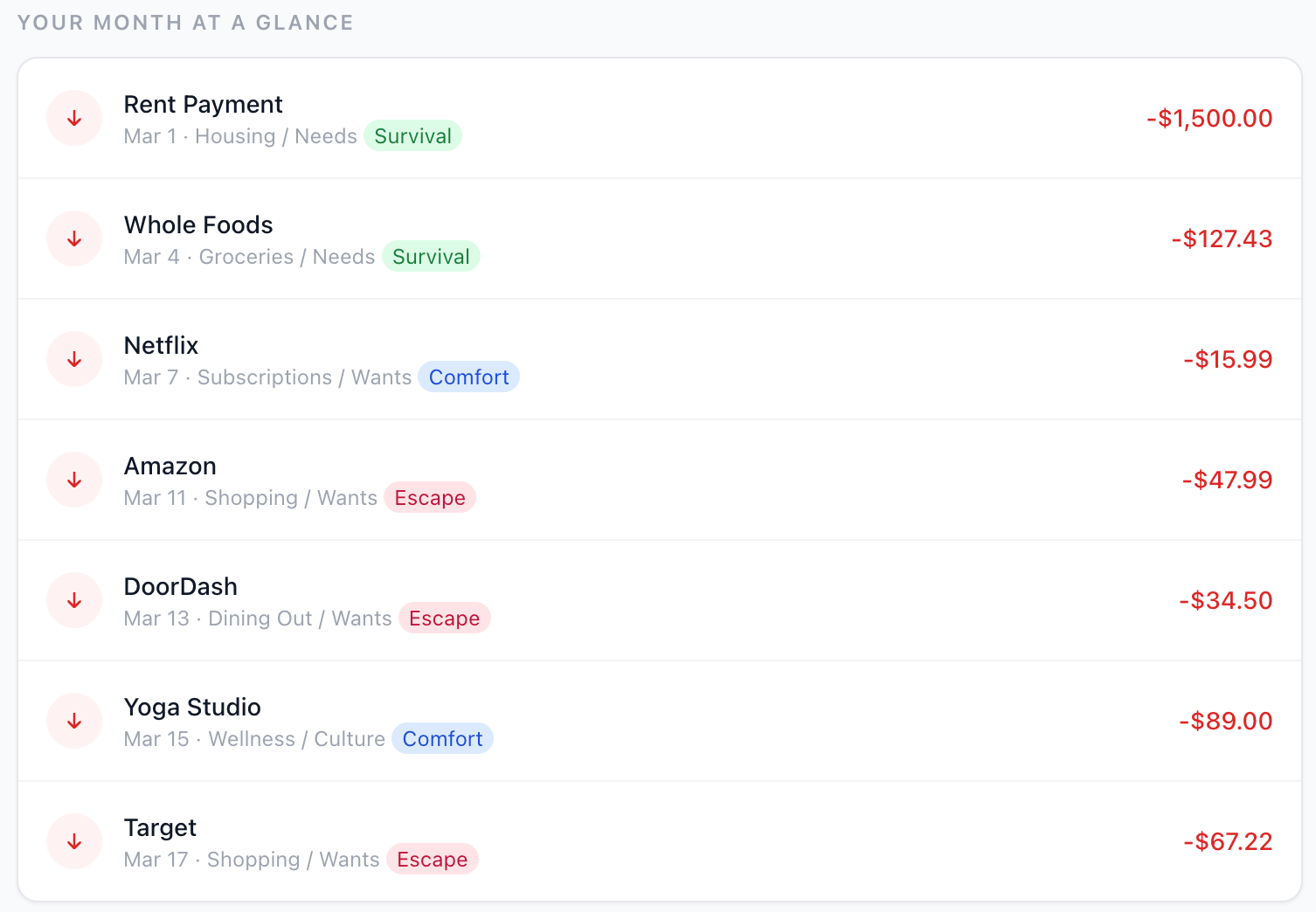

The transaction list makes it even more visceral. You scroll through your month and the little colored badges tell the story. Green, green, blue, green, red, red, red. Three Escape purchases in a row on a Wednesday evening. You don’t need a financial advisor to tell you what happened that Wednesday. You already know.

This Isn’t About Elimination

I want to be clear about something, because I’ve seen this misread: the goal is not to eliminate Escape spending. The goal is to see it.

Some Escape spending is fine. You had a terrible day and a $6 coffee made you feel human again. That’s a reasonable exchange. The problem isn’t any individual purchase; it’s the pattern you can’t see without the data. When Escape spending creeps from 10% to 15% to 24% over a few months, that’s a signal worth noticing. Not because you’re bad with money, but because something in your life is generating stress that you’re paying Amazon, Starbucks, etc. to absorb.

The Mindful Tags report doesn’t prescribe. It describes. “This is what happened. This is how your money moved. Here’s the emotional texture of those movements.” What you do with that information is up to you.

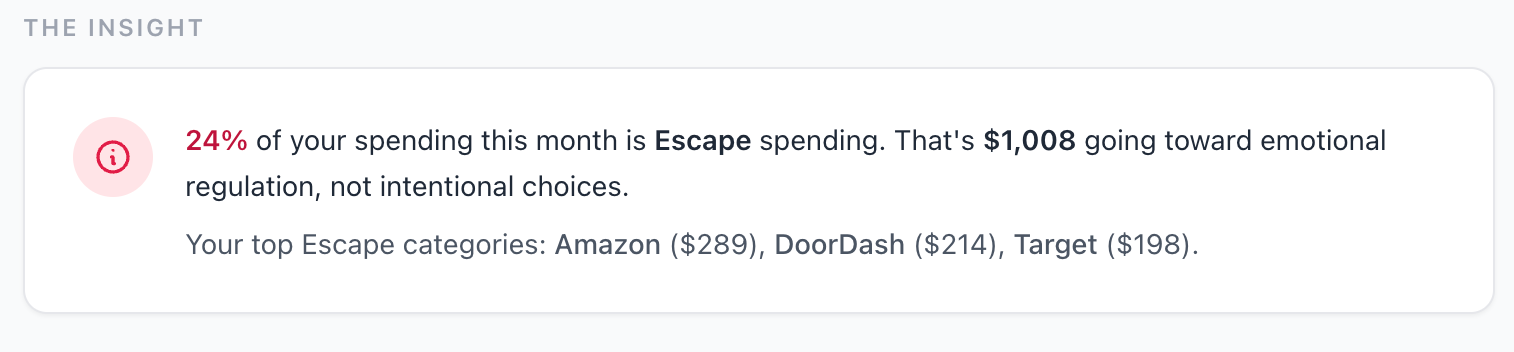

The insight card at the bottom is where it lands. Plain language, no judgment, specific numbers. Your top Escape categories, the dollar amounts, the percentage. Data you can act on or data you can sit with. Either way, you’re no longer unconscious about it.

Why This Matters for Financial Literacy

Financial literacy programs love to teach people about compound interest and index funds and the time value of money. That’s fine. Those concepts matter. Heck, they’re some of my favorite subjects to teach about. But they’re downstream of a more fundamental problem: most people don’t understand their own spending patterns well enough to have money left over to invest in the first place.

Survival/Comfort/Escape is a framework that meets people where they actually are. Not “here’s how a 401k works” but “here’s what’s happening with the money you already spend every day.” That’s the starting line. Everything else — budgeting, saving, investing, debt payoff — comes after you can see clearly where your money goes and why it goes there.

I need to say something about shame cycles here, too. Shame is a significant presence in my own life. Shame creeps up for me around unfinished projects, the untidy workbench in the garage, when I have to say “no” to somebody when they ask for my help. I’m currently stuck in two overlapping shame cycles in regards to some interpersonal conflict with friends.

I’m no therapist or psychologist, but I know that for myself, the most important part of breaking my shame cycles is to first recognize the pattern. I know that I develop shame around those unfinished projects because I simply take on too many projects, which later leads me to having to say “no” when the next person needs my help because I’m so backlogged and lacking capacity.

In order to regulate my nervous system and avoid this shame cycle, I actually need to say “no” more often, so that I don’t get backlogged, bogged down, and energetically shut down and socially isolate. The “no” needs to precede the start of the shame cycle, so that I can protect my energy and have the capacity for a “yes” when the request is in alignment with the work I want to be doing and the people I want to serve.

I think it’s similar with money. It’s hard to look at our spending patterns in the way described above, and for some people it might trigger a shame cycle. I’m sure an expert will correct me in the comments if I’m wrong, but I believe that in order to prevent future shame cycles, we need to see the pattern that triggers them in the first place.

Awareness and recognition then generates the plan for regulation. We can’t discuss our disregulated spending with our financial coach or therapist if we’re not aware of the pattern. Without knowing there’s a pattern, and the exact extent of it in real dollar terms, we can’t take action to course correct. As famed management analyst Peter Drucker said, “What gets measured gets managed.” This is the measurement.

So it is my hope that this unique feature in Heartfelt Finance will be the start of pattern recognition and regulation for you, if it’s something you’re in need of on the financial front.

So there you have it. The three-button tag takes two seconds. The monthly donut chart takes thirty seconds to read. And the pattern it reveals is worth more than any financial literacy course I’ve ever seen, because it’s built from your actual life, not a textbook scenario.

Tag your spending for one month. Just one. Then look at the donut chart. I promise you’ll see something you didn’t expect.

Heartfelt Finance is free for individual users. It’s a budgeting tool, spending tracker, goal planner, investment tracker, credit score education tool, and the like — but built around money mindfulness. Check it out at https://HeartfeltFinance.com.